Select Between a Private Mortgage and a Line of Credit score

Associated Articles

- The Influence Of Federal Reserve Fee Hikes On Private Loans: Navigating The Shifting Panorama

- Navigating The Mortgage Panorama: A Complete Information To Evaluating Private Mortgage Gives

- Can You Use A Private Mortgage To Pay Off Medical Payments? A Complete Information

- Understanding the Influence of Mortgage Curiosity Charges on Month-to-month Budgets

- Prime 5 Private Mortgage Suppliers In The U.S. For 2024

Introduction

Uncover all the pieces it’s essential to learn about Select Between a Private Mortgage and a Line of Credit score

Video about

Private Mortgage vs. Line of Credit score: Which One’s Proper for You?

Life throws curveballs. Typically, you want a little bit additional money to deal with sudden bills, fund a dream venture, or consolidate debt. When that occurs, you may end up weighing the professionals and cons of a private mortgage and a line of credit score. Each supply monetary flexibility, however understanding their key variations may help you select the choice that most closely fits your wants.

Understanding the Fundamentals

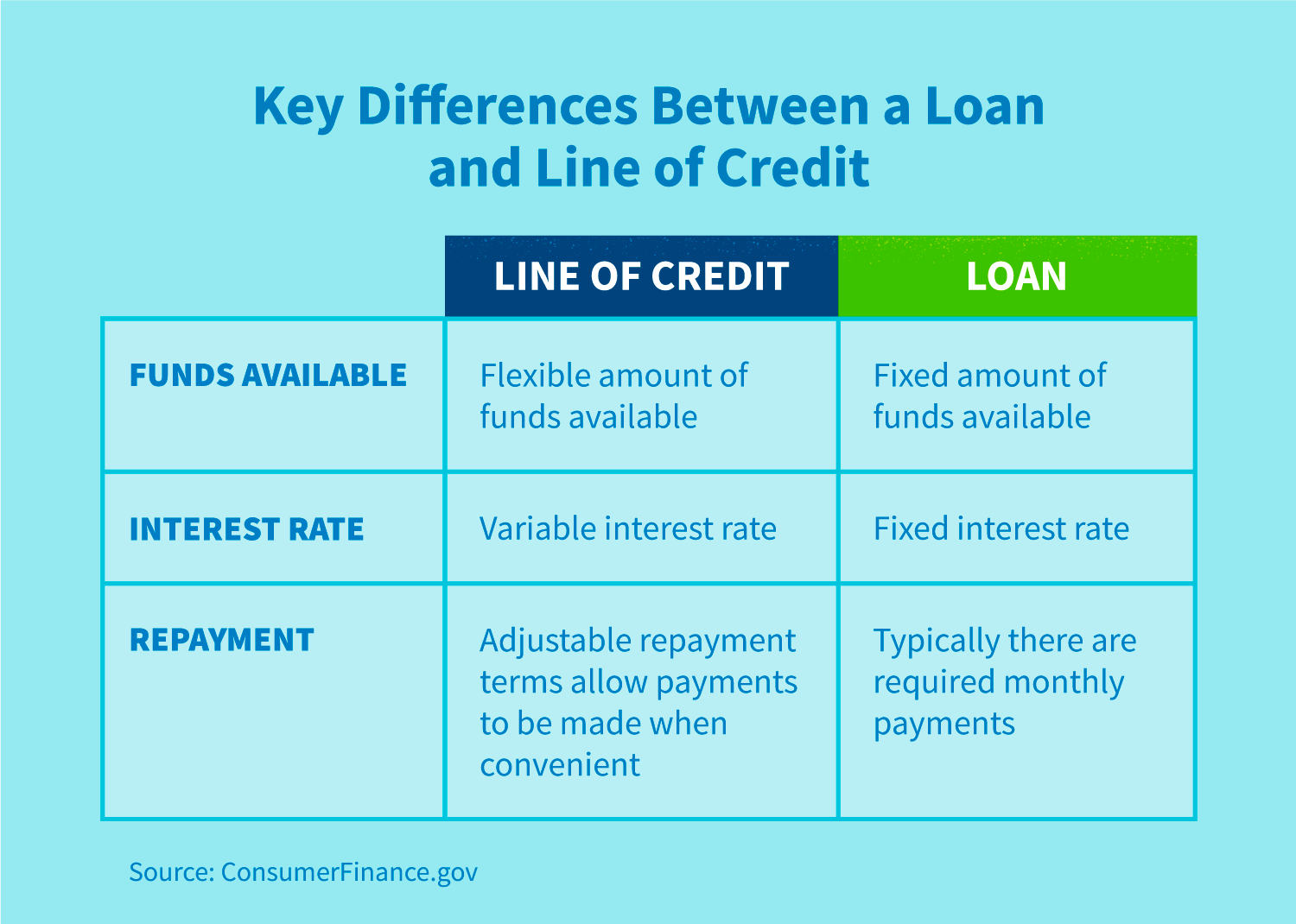

- Private Mortgage: A private mortgage is a hard and fast sum of cash you borrow at a set rate of interest for a selected time period. Consider it as a one-time injection of money that you just repay in common installments.

- Line of Credit score: A line of credit score is a revolving credit score account that provides you entry to a pre-approved sum of money, often known as your credit score restrict. You may borrow as a lot as you want, as much as your restrict, and repay the borrowed quantity over time.

Key Variations: A Head-to-Head Comparability

1. Entry to Funds:

- Private Mortgage: You obtain the complete mortgage quantity upfront, making it ultimate for big, one-time bills like a brand new automotive or dwelling renovations.

- Line of Credit score: You will have entry to a pre-approved quantity, permitting you to borrow what you want if you want it, making it good for smaller, recurring bills or sudden emergencies.

2. Reimbursement:

- Private Mortgage: You repay the mortgage in fastened month-to-month installments over a set time period, usually starting from 12 to 84 months. This predictable reimbursement construction helps you funds successfully.

- Line of Credit score: You solely pay curiosity on the quantity you borrow, and you’ve got the pliability to make minimal funds or repay the steadiness in full at any time. This flexibility could be helpful you probably have fluctuating earnings or have to handle money movement.

3. Curiosity Charges:

- Private Mortgage: Rates of interest on private loans are usually fastened, that means they continue to be the identical all through the mortgage time period. This predictability helps you intend your funds.

- Line of Credit score: Rates of interest on strains of credit score are normally variable, that means they will fluctuate with market circumstances. This could make it tough to foretell your month-to-month funds, particularly in periods of rising rates of interest.

4. Charges:

- Private Mortgage: Private loans might include origination charges, that are charged upfront to cowl the lender’s administrative prices.

- Line of Credit score: Strains of credit score might have annual charges, inactivity charges, or money advance charges, relying on the precise phrases of the settlement.

5. Credit score Influence:

- Private Mortgage: A private mortgage can positively influence your credit score rating for those who make well timed funds. It may well additionally assist enhance your credit score utilization ratio, which is the share of your obtainable credit score you are utilizing.

- Line of Credit score: A line of credit score can negatively influence your credit score rating for those who use a good portion of your obtainable credit score, as it could actually improve your credit score utilization ratio. Nevertheless, for those who use it responsibly and pay it off in full every month, it could actually positively influence your credit score rating.

Selecting the Proper Choice: A Sensible Information

1. Outline Your Monetary Wants:

- Giant, One-Time Bills: For those who want a major sum of money for a single buy, a private mortgage is probably going the higher alternative.

- Smaller, Recurring Bills: For smaller, ongoing bills or sudden emergencies, a line of credit score supplies better flexibility.

2. Assess Your Monetary Scenario:

- Credit score Rating: A great credit score rating typically results in decrease rates of interest on each private loans and contours of credit score.

- Debt-to-Earnings Ratio: A decrease debt-to-income ratio (DTI) makes you a extra enticing borrower and can lead to extra favorable mortgage phrases.

- Earnings Stability: In case your earnings is predictable, a private mortgage with fastened funds could be a greater possibility. In case your earnings fluctuates, a line of credit score’s versatile reimbursement construction may very well be extra helpful.

3. Examine Mortgage Phrases:

- Curiosity Charges: Examine rates of interest from a number of lenders to seek out probably the most aggressive supply.

- Charges: Think about any origination charges, annual charges, or different costs related to the mortgage.

- Reimbursement Phrases: Select a mortgage time period that matches your funds and reimbursement capabilities.

4. Perceive the Dangers:

- Overspending: With a line of credit score, it is easy to overspend for those who’re not cautious. Set spending limits and follow them.

- Variable Curiosity Charges: Variable rates of interest on strains of credit score can improve your month-to-month funds, making it tough to funds.

- Credit score Rating Influence: Utilizing a good portion of your obtainable credit score on a line of credit score can negatively influence your credit score rating.

Private Mortgage: When it Makes Sense

- Main Purchases: New automotive, dwelling renovations, medical bills, or debt consolidation.

- Predictable Earnings: Common, constant earnings makes fastened month-to-month funds manageable.

- Good Credit score Rating: A great credit score rating typically results in decrease rates of interest.

Line of Credit score: When it Makes Sense

- Surprising Bills: Medical payments, automotive repairs, or dwelling emergencies.

- Fluctuating Earnings: Versatile reimbursement choices may help handle money movement in periods of earnings instability.

- Brief-Time period Wants: For bills you anticipate to repay shortly, a line of credit score is usually a cost-effective possibility.

Examples of When to Select Every Choice

Private Mortgage:

- State of affairs: You are planning a house renovation venture estimated to price $20,000. You will have a gradual earnings and an excellent credit score rating.

- Resolution: A private mortgage with a hard and fast rate of interest and a 5-year time period would give you the mandatory funds and a predictable reimbursement construction.

Line of Credit score:

- State of affairs: You are a contract author with fluctuating earnings. You want entry to a small sum of money to cowl sudden bills like medical payments or automotive repairs.

- Resolution: A line of credit score with a low credit score restrict and variable rate of interest would give you the pliability to borrow solely what you want and make funds based mostly in your earnings.

Further Ideas for Success

- Store Round: Examine provides from a number of lenders to seek out the perfect charges and phrases.

- Learn the Nice Print: Perceive all of the charges and phrases earlier than signing any mortgage settlement.

- Funds Correctly: Create a practical funds that features your mortgage funds to keep away from overspending.

- Pay on Time: Making well timed funds is essential for sustaining an excellent credit score rating and avoiding late charges.

- Monitor Your Spending: Observe your spending to make sure you’re utilizing your line of credit score responsibly.

Conclusion

Selecting between a private mortgage and a line of credit score is dependent upon your particular monetary wants, credit score rating, and earnings stability. By fastidiously contemplating the professionals and cons of every possibility, you may make an knowledgeable resolution that most closely fits your state of affairs and helps you obtain your monetary targets. Bear in mind, accountable borrowing and monetary planning are key to maximizing the advantages of each private loans and contours of credit score.

Closure

We hope this text has helped you perceive all the pieces about Select Between a Private Mortgage and a Line of Credit score. Keep tuned for extra updates!

Don’t overlook to examine again for the newest information and updates on Select Between a Private Mortgage and a Line of Credit score!

Be at liberty to share your expertise with Select Between a Private Mortgage and a Line of Credit score within the remark part.

Keep knowledgeable with our subsequent updates on Select Between a Private Mortgage and a Line of Credit score and different thrilling subjects.