Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected

Related Articles

- How Do Personal Loans Affect Your Credit Score? A Comprehensive Guide

- Unlocking Your Financial Potential: A Guide To Responsible Personal Loan Borrowing

- Personal Loan Calculator: How Much Can You Afford To Borrow?

- Personal Loans Vs. Payday Loans: Which Should You Choose?

- Prime 5 Private Mortgage Suppliers In The U.S. For 2024

Introduction

Uncover the latest details about Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected in this comprehensive guide.

Video about

Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected

Getting a personal loan can be a lifeline for many, offering financial flexibility to consolidate debt, cover unexpected expenses, or fund exciting projects. But the reality is, not every application gets approved. Rejection can feel like a blow, leaving you feeling frustrated and uncertain.

Don’t despair! While a rejection can be disheartening, it’s not the end of the road. Understanding why your application was denied and taking proactive steps can increase your chances of securing the loan you need in the future.

This comprehensive guide will walk you through the process of navigating a personal loan rejection, providing actionable steps and valuable insights to help you get back on track.

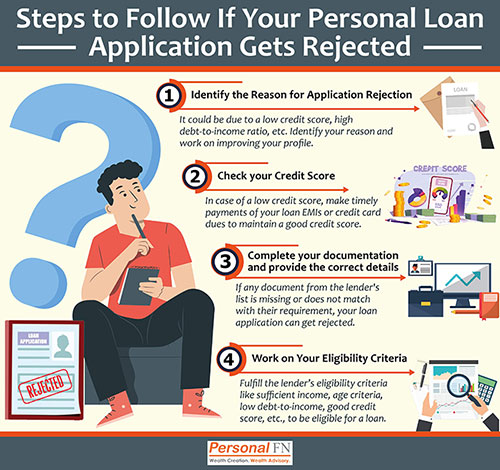

Understanding the Reasons for Rejection

The first step to overcoming a loan rejection is understanding the reasons behind it. Lenders use a variety of factors to assess your creditworthiness, and a rejection often signals an issue with one or more of these areas.

1. Credit Score and History

Your credit score is a crucial factor in loan approval. A low credit score, reflecting a history of missed payments or excessive debt, can raise red flags for lenders.

2. Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your monthly income that goes towards debt payments. A high DTI can indicate a strain on your finances, making lenders hesitant to approve a new loan.

3. Income and Employment History

Lenders want to ensure you have a stable income source to make loan repayments. A lack of consistent employment history or low income can lead to rejection.

4. Loan Amount and Purpose

The amount you’re requesting and the purpose of the loan are also considered. Lenders may be reluctant to approve loans for high amounts or those with unclear purposes.

5. Recent Credit Inquiries

Multiple recent credit inquiries can negatively impact your credit score, as they indicate frequent loan applications, potentially signaling financial distress.

6. Negative Credit Entries

Past bankruptcies, foreclosures, or collections can significantly damage your credit score and make it difficult to secure a loan.

7. Insufficient Collateral

For secured loans, lenders require collateral, such as a car or home, to secure the loan. If the collateral is deemed insufficient or lacks value, your application may be rejected.

8. Age and Residency

While not always a deciding factor, your age and residency may play a role in loan approval, particularly for certain lenders or loan types.

9. Bankruptcy or Foreclosure History

Having a history of bankruptcy or foreclosure can significantly impact your credit score and make it difficult to secure a loan.

10. Insufficient Savings

Lenders may consider your savings history as an indicator of your financial stability. Insufficient savings can raise concerns about your ability to repay the loan.

11. Lack of Financial History

If you are new to credit or have limited financial history, lenders may be hesitant to approve a loan due to insufficient information about your creditworthiness.

12. Recent Negative Events

Recent events, such as a job loss or a medical emergency, can impact your financial situation and make lenders hesitant to approve a loan.

Taking Action After Rejection

Once you understand the reasons behind the rejection, it’s time to take action. Don’t let the initial setback discourage you.

1. Review Your Credit Report and Score

Request a free copy of your credit report from all three major credit bureaus: Experian, Equifax, and TransUnion. Review the report for any errors or inaccuracies that could be affecting your score.

2. Dispute Errors on Your Credit Report

If you find any errors on your credit report, dispute them with the credit bureau and the original creditor. Correcting errors can significantly improve your score and increase your chances of loan approval.

3. Improve Your Credit Score

Focus on improving your credit score by making timely payments on all your debts, keeping your credit utilization low, and avoiding unnecessary credit applications.

4. Reduce Your Debt

Pay down existing debt to lower your DTI and improve your credit score. Consider strategies like debt consolidation or balance transfers to manage your debt more effectively.

5. Increase Your Income

If your income is low, consider taking on a side hustle or looking for a higher-paying job to improve your financial stability and increase your chances of loan approval.

6. Save for a Down Payment

For secured loans, aim to save for a larger down payment to minimize the loan amount and improve your chances of approval.

7. Consider a Co-signer

If you’re struggling to qualify for a loan, consider asking a trusted individual with good credit to co-sign the loan. A co-signer’s creditworthiness can help offset your own credit history.

8. Explore Alternative Loan Options

If you’re still facing rejection, explore alternative loan options such as:

- Peer-to-peer (P2P) lending: P2P lending platforms connect borrowers with individual investors, often offering more flexible terms and lower interest rates.

- Credit unions: Credit unions often have more lenient lending requirements than traditional banks, making them a good option for borrowers with less-than-perfect credit.

- Online lenders: Online lenders offer quick and convenient loan options, but it’s essential to compare interest rates and terms carefully.

- Secured loans: Secured loans use an asset, such as a car or home, as collateral, which can improve your chances of approval, even with a lower credit score.

9. Negotiate With the Lender

If your application was rejected due to a specific reason, try to negotiate with the lender. Explain your situation and see if there are any alternative options or solutions available.

10. Re-apply After Improving Your Finances

After taking steps to improve your credit score, reduce debt, or increase income, consider reapplying for the loan. Be prepared to provide updated financial documentation to demonstrate your improved financial standing.

11. Seek Professional Financial Advice

If you’re struggling to navigate the loan application process or need help improving your financial situation, consider seeking professional financial advice from a credit counselor or certified financial planner.

12. Consider a Credit Builder Loan

Credit builder loans can be helpful for individuals with limited credit history or low credit scores. These loans require borrowers to make regular payments, which are then reported to the credit bureaus, helping to build credit.

13. Build a Relationship with a Local Lender

Developing a relationship with a local lender can be beneficial. By demonstrating your financial responsibility and commitment to responsible borrowing, you can increase your chances of approval in the future.

14. Shop Around for Different Lenders

Don’t settle for the first lender that rejects you. Shop around and compare offers from different lenders to find the best rates and terms.

15. Be Patient and Persistent

Improving your credit score and financial situation takes time and effort. Be patient, persistent, and stay focused on your financial goals.

Tips for Avoiding Rejection in the Future

Once you’ve overcome the initial rejection, it’s important to learn from the experience and take steps to avoid future rejections.

- Monitor your credit score regularly: Check your credit score at least once a month to ensure it’s in good standing.

- Pay bills on time: Make all payments on time to avoid late fees and negative credit entries.

- Keep credit utilization low: Aim to keep your credit utilization ratio below 30%.

- Avoid unnecessary credit applications: Only apply for credit when you truly need it.

- Budget carefully: Create a budget and stick to it to manage your finances effectively.

- Save regularly: Set aside money for emergencies and future financial needs.

- Build an emergency fund: Having an emergency fund can help you avoid taking on unnecessary debt in the future.

- Seek financial counseling: If you’re struggling to manage your finances, consider seeking professional financial advice.

Conclusion

Getting a personal loan rejected can be a frustrating experience, but it’s not the end of the road. By understanding the reasons behind the rejection, taking proactive steps to improve your credit score and financial situation, and exploring alternative loan options, you can increase your chances of securing the loan you need in the future.

Remember, building good credit takes time and effort. By being patient, persistent, and committed to responsible financial management, you can achieve your financial goals and navigate the loan application process with confidence.

Closure

Thank you for reading! Stay with us for more insights on Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected.

Don’t forget to check back for the latest news and updates on Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected!

We’d love to hear your thoughts about Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected—leave your comments below!

Stay informed with our next updates on Loan Denied? Don’t Panic! Here’s What to Do When Your Personal Loan Application Gets Rejected and other exciting topics.